Saving money doesn’t have to be an exhausting, uphill battle. In fact, if you are constantly struggling to stash away cash at the end of the month, you are likely relying on the wrong strategy. For many people, the idea of saving money sounds like a chore. You tell yourself that you will save whatever is left over after all your expenses are paid. But somehow, there is never anything left. Unexpected bills, daily coffees, weekend takeout, and impulse online shopping seem to drain your checking account before your savings even have a chance to grow.

This is where the magic of financial automation comes into play. By creating a system that removes willpower from the equation, you can make saving completely effortless. When you automate your transfers, bill payments, and even roundups from everyday purchases, you set yourself up for long-term financial success without the constant stress of manual budgeting. Building wealth is not about making massive, one-time sacrifices; it is about designing a frictionless environment where your money works for you in the background.

In this comprehensive guide, we will explore the step-by-step process of putting your personal finances on autopilot. From shifting your money mindset to leveraging modern micro-investing apps, you will learn exactly how to build a robust financial safety net. Whether you are looking for beginner investing tips, budgeting hacks, or passive income ideas, mastering automation is the foundational step that makes everything else possible. Let us dive into the ultimate blueprint for effortless wealth building.

The Psychology of Saving: Why Willpower Fails

Before we set up any technical bank transfers, it is crucial to understand the psychology behind why manual saving fails. Human beings are not naturally wired to delay gratification. We are biologically programmed to seek immediate rewards, which makes resisting the temptation to spend incredibly difficult. When you rely on willpower to save money, you are fighting against your own brain chemistry every single day.

Willpower is like a muscle; it gets fatigued as the day goes on. You might start the month with strong intentions, but after a long, stressful day at work, your decision-making energy is depleted. That is when the impulse to order expensive delivery or buy something you do not need takes over. Relying on discipline and memory to manage your finances is a recipe for inconsistency. Life gets busy, emergencies happen, and your savings goals get pushed to the back burner.

Automation solves this psychological flaw entirely. By taking the decision-making process out of your daily routine, you bypass the need for willpower altogether. You are essentially tricking your brain into saving by making the process invisible. Once the system is running, you no longer have to ask yourself, “Can I afford to save this month?” The decision has already been made for you. This fundamental shift from active resistance to passive accumulation is the cornerstone of modern personal finance.

Step 1: The Mindset Shift – Pay Yourself First

The very first step to financial automation is a profound mindset shift. You must accept one universal truth of personal finance: saving does not happen by accident. If you wait until the end of the month to see what is left over, chances are you will save absolutely nothing. The traditional approach to budgeting dictates that Income – Expenses = Savings. This formula is fundamentally flawed because it treats savings as an afterthought.

To build wealth, you must flip the script and adopt the “Pay Yourself First” philosophy. The new, wealth-building formula is Income – Savings = Expenses. When your paycheck hits your account, your automated system immediately routes a predetermined percentage into your savings and investment accounts. You then live your life, pay your bills, and enjoy your guilt-free spending money using whatever is left over.

This simple mindset shift is the absolute foundation of financial security. It ensures that your future self is always prioritized over your present desires. You are no longer sacrificing your lifestyle to save; instead, you are adjusting your lifestyle to fit the money that remains after your wealth-building contributions are made. Over time, this mental accounting reshapes your relationship with money, making saving the default option and overspending the exception.

Step 2: Create a Fortress for Your Wealth – Separate Accounts

Once your mindset is aligned, the next practical step is to create a dedicated savings account. Ideally, this should be a high-yield savings account located at a completely different financial institution than your everyday checking account. Why is this separation so important? Because proximity breeds temptation.

When your savings are sitting in the same account you use to pay for groceries, dinners out, and online shopping, the money feels entirely accessible. You see a large balance and your brain registers it as “available to spend.” Having a separate account at a different bank creates a psychological barrier. The money feels less accessible, almost as if it is locked away in a vault. Furthermore, using an out-of-sight bank means you will not see your savings balance every time you log in to check your checking account for daily spending, reducing the urge to dip into it.

To stay motivated, take advantage of the customization features offered by modern online banks. You can nickname your accounts based on your specific financial goals. Label them “Emergency Fund,” “Dream Vacation,” “First Home Down Payment,” or “Financial Freedom.” Seeing these specific names attached to your growing balances provides a constant visual reminder of why you are saving, keeping your long-term goals at the forefront of your mind.

Step 3: Timing is Everything – Automating Transfers

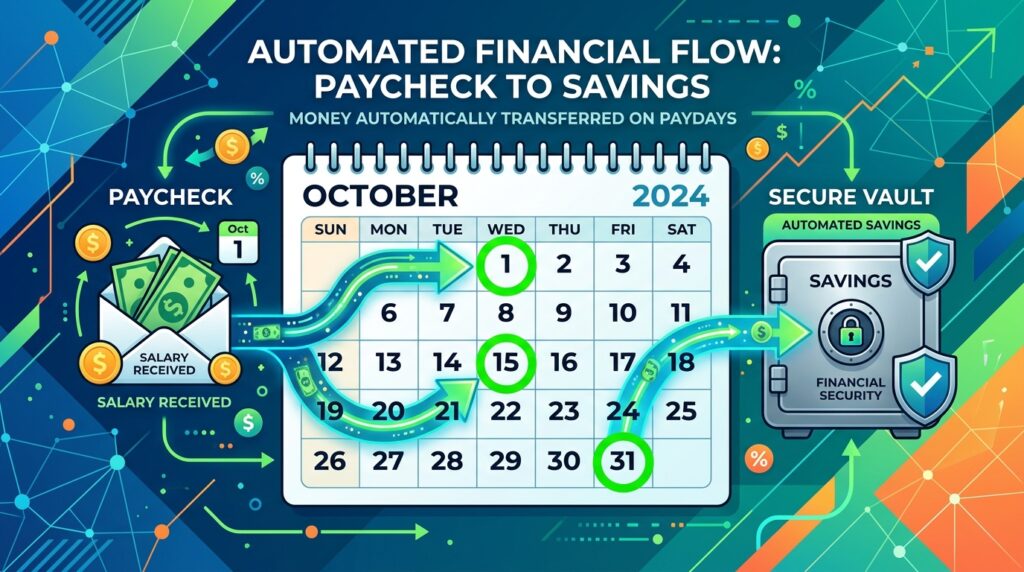

The real magic of personal finance automation begins when you set up recurring transfers from your checking account to your newly established savings accounts. Most banks, credit unions, and financial apps allow you to schedule these deposits for specific days of the month, and timing is critical to your success.

The most effective strategy is to time your automated transfers to coincide exactly with your payday. If you receive your paycheck on the 1st and the 15th of every month, set up your automatic savings transfers to execute on those exact same days, or perhaps one day later to allow for clearing. By moving the money before you even have a chance to look at it, you ensure that your savings are funded first.

Do not worry if you cannot afford to automate massive transfers right away. The key to this strategy is consistency, not perfection. Even if you can only afford to automate $25 or $50 per paycheck, the habit is what matters most. Over time, as your income grows or your expenses decrease, you can simply log into your banking portal and increase the automated transfer amount. These small, consistent deposits act like a financial snowball, rolling downhill and gathering mass until they turn into tens of thousands of dollars, all without requiring any active thought on your part.

Step 4: The Power of Savings Buckets – Goal-Based Saving

Saving becomes exponentially more powerful and motivating when you give every single dollar a specific job. Instead of throwing all of your hard-earned money into one giant, general savings account, divide it across multiple “buckets” or sub-accounts based on your distinct financial goals.

For example, you might set up automatic transfers into three separate funds: $200 a month for your emergency fund, $100 for a travel fund, and $50 for holiday gifts or a new car. Watching each individual goal grow at its own pace provides a massive psychological boost. When you hit a milestone in your travel fund, you feel a sense of accomplishment that motivates you to keep contributing, even if your emergency fund is growing a bit slower.

Many modern financial technology platforms make this strategy incredibly easy to implement. Online banks and budgeting applications allow you to create virtual sub-accounts or digital savings buckets within a single master account. This allows you to track your progress toward multiple goals simultaneously without the hassle of managing a dozen different bank logins. By segmenting your savings, you ensure that a surprise car repair does not accidentally drain the money you had earmarked for your summer vacation.

Step 5: Protect Your Foundation – Automating Bills

An automated savings strategy only works effectively if your outgoing cash flow is also on autopilot. You cannot build a strong financial house on a cracked foundation. Late fees, missed payments, overdraft charges, and sudden drops in your credit score can quickly wipe out the progress you have made in your savings accounts.

To protect your wealth, you must set up autopay for all of your essential fixed expenses. This includes your rent or mortgage, utility bills, car insurance, internet, and minimum credit card payments. By automating your bills, you ensure that your financial foundation remains rock solid while your savings grow in the background.

Beyond the financial protection, automating your bills provides immense mental relief. Financial stress often stems from the cognitive load of remembering due dates, writing checks, and worrying about whether a payment went through on time. When your essential bills are paid automatically, you free up valuable mental bandwidth. You will never again have to scramble to remember a due date or experience the sinking feeling of realizing you missed a payment. Automation protects your money both coming in and going out, creating a seamless, stress-free financial ecosystem.

Step 6: Micro-Saving Magic – Roundup Apps

Technology has revolutionized the way we interact with our money, making saving entirely effortless through the use of roundup applications. These innovative apps connect to your debit and credit cards and automatically round up your everyday purchases to the nearest dollar.

For instance, if you buy a cup of coffee for $4.50, the app rounds the transaction up to $5.00 and automatically transfers the extra $0.50 into a dedicated savings or micro-investment account. While fifty cents might seem insignificant in the moment, these micro-transactions accumulate incredibly fast. Over the course of a year, the spare change from your daily habits can add hundreds of dollars to your net worth without you ever noticing the money leaving your primary checking account.

Apps designed for micro-savings act like a digital piggy bank that works tirelessly in the background. Some of these platforms even use algorithms to analyze your spending habits and safely sweep small, affordable amounts into your savings account a few times a week. This approach to passive income and saving is perfect for beginners who feel they do not have enough money to start a traditional investment portfolio. It proves that building wealth is not just about the size of your income, but the consistency of your saving habits.

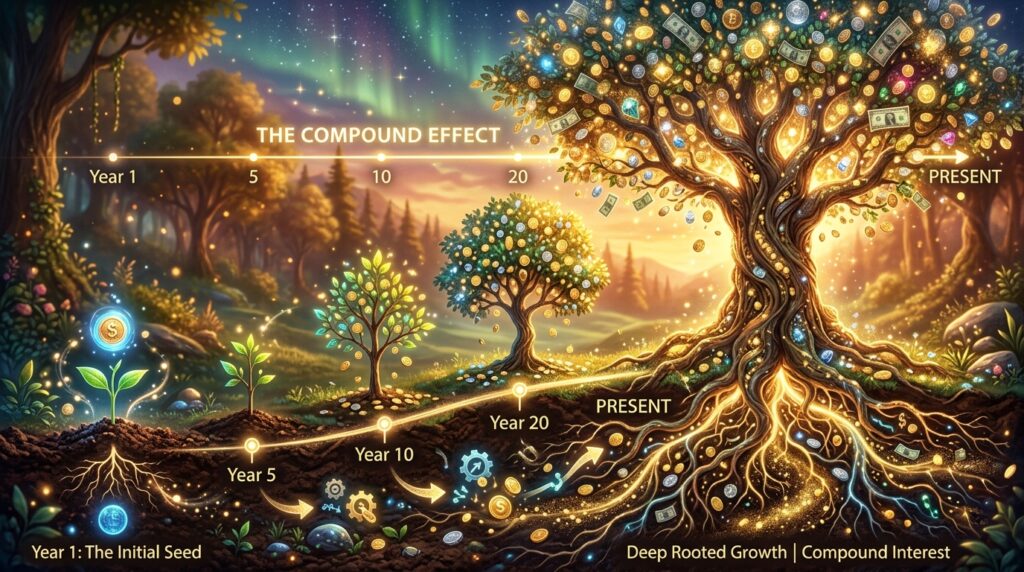

Step 7: The Compound Effect – Consistency and Silent Growth

Consistency is the undisputed secret ingredient to building long-term wealth, and automation is the absolute easiest way to guarantee that consistency. When you attempt to save manually, you are relying on discipline, memory, and motivation—three things that inevitably fluctuate. But once your automatic transfers are locked in, consistency is mathematically guaranteed. Whether you are feeling highly motivated or completely burnt out that month, the money still moves into your savings and investment accounts.

This steady, unbreakable stream of deposits harnesses the most powerful force in personal finance: the compound effect. Wealth is rarely built through occasional, massive efforts or lucky windfalls. It is built through small, consistent actions repeated relentlessly over years and decades. Think of it like going to the gym; physical transformation does not come from one intense, exhausting workout. It comes from showing up regularly, week after week.

The magic of automatic savings is that it feels entirely invisible at first. You may not notice those small, automated transfers leaving your account every week. But when you check your balance after six months, a year, or five years, you will be genuinely shocked at how much you have accumulated. This silent growth builds incredible momentum and confidence. For example, someone automating a transfer of just $100 a month into an index fund yielding an average historical return will have a substantial nest egg in ten years. That sense of tangible progress encourages you to keep going, proving that financial security is entirely within your reach.

Step 8: Automation as Your Ultimate Financial Secret Weapon

At the heart of all successful personal finance strategies lies one core concept: automation is your ultimate secret weapon. It takes the hardest, most emotionally taxing part of money management—self-control—completely out of the equation. You no longer have to agonize over whether to save or spend, because the decision was made by you, for you, months ago.

This simple systemic shift turns saving into a deeply ingrained habit that requires zero mental effort, freeing you to focus on what truly matters: living your life, advancing your career, and spending time with loved ones. Whether your current goal is building a robust emergency fund, saving for a dream vacation, aggressively paying down high-interest debt, or preparing for a comfortable retirement, automation ensures steady, mathematical progress without the constant anxiety of manual budgeting.

Financial experts and wealthy individuals consistently recommend automation because it scales with your life. As your career advances and your income increases, you simply adjust the percentages in your automated system. You do not have to work harder to save more; your system simply captures more of your growing wealth. It is not about how much willpower you can muster today; it is about building an unbreakable system that keeps working for you tomorrow, next year, and decades into the future.

Beyond Saving: Transitioning to Automated Investing

While automating your savings accounts is the perfect starting point, true wealth generation requires moving beyond cash savings and stepping into the world of automated investing. Once your emergency fund is fully funded and your high-interest debt is eliminated, you must redirect your automated transfers into income-producing assets.

Just as you can automate transfers to a high-yield savings account, you can set up automatic monthly contributions to a brokerage account or a retirement fund like a Roth IRA. By utilizing automated investing platforms, often referred to as robo-advisors, you can build a diversified portfolio of low-cost index funds without needing to be a stock market expert. These platforms automatically rebalance your portfolio and reinvest your dividends, ensuring that your money is constantly working to generate passive income.

Treating your investment contributions as a non-negotiable monthly bill is the ultimate budgeting hack. You are effectively buying your future freedom one automated transaction at a time. By combining the psychological benefits of automated saving with the mathematical power of automated investing, you create a dual-engine wealth-building machine that operates flawlessly while you sleep.

Conclusion

The secret to saving more money and building lasting wealth is not found in extreme frugality or superhuman willpower. It is found in the intelligent application of automation. By setting up automatic transfers, segmenting your goals into digital buckets, automating your essential bills, and leveraging micro-saving technology, you remove the friction and temptation that typically derail financial plans. You transition from actively fighting against your spending impulses to passively accumulating wealth in the background.

Taking control of your personal finances does not require you to become a spreadsheet wizard or a Wall Street expert. It simply requires you to design a system that aligns with your goals and then let technology do the heavy lifting. Start small, set up your first automated transfer today, and watch as your financial safety net grows stronger with every passing month. Your future self will thank you for making the smart, effortless choice.

Frequently Asked Questions (FAQ)

1. How much money should I automate into my savings account every month?

The ideal amount to automate depends entirely on your income, expenses, and financial goals. A popular budgeting rule of thumb is the 50/30/20 rule, which suggests allocating 20% of your after-tax income toward savings and debt repayment. However, if you are just starting out, do not let perfection be the enemy of progress. Automating even $25 or $50 per paycheck is enough to build the habit. The most important factor is consistency; you can always increase the automated amount later as your income grows or your expenses decrease.

2. Will automating my savings cause me to overdraft my checking account?

This is a common concern, but it is easily managed. To prevent overdrafts, ensure that your automated transfers are scheduled to occur a day or two after your paycheck has fully cleared in your checking account. Additionally, keep a small “buffer” of extra cash in your checking account to absorb minor fluctuations in your daily spending. Many modern banking apps also offer low-balance alerts or automatic transfer pausing features if your checking account drops below a certain threshold, providing an extra layer of safety.

3. What is the difference between a high-yield savings account and a standard savings account?

A standard savings account, typically offered by traditional brick-and-mortar banks, usually pays a very low interest rate, often less than 0.10% annually. A high-yield savings account (HYSA), usually offered by online banks, pays a significantly higher interest rate—often 10 to 20 times higher than a standard account. When automating your savings, it is highly recommended to use an HYSA. Because online banks have lower overhead costs, they pass those savings on to you in the form of higher yields, allowing your automated deposits to grow much faster through the power of compound interest.

4. Can I automate my investments the same way I automate my savings?

Absolutely. In fact, automating your investments is one of the most powerful wealth-building strategies available. You can set up recurring, automatic transfers from your checking account directly into a brokerage account, a traditional IRA, or a Roth IRA. Many brokerages also offer “automatic investment plans” that allow you to automatically purchase fractional shares of specific stocks, mutual funds, or exchange-traded funds (ETFs) on a set schedule. This strategy, known as dollar-cost averaging, helps smooth out market volatility over time.

5. Are micro-saving and roundup apps actually worth using?

Yes, micro-saving and roundup apps are highly effective, particularly for beginners or those who struggle with traditional budgeting. While the individual transactions are small, the psychological benefit is massive. These apps capitalize on “mental accounting” by hiding the savings process in the background. You do not feel the pain of parting with the money because it is just spare change. Over the course of a year, these roundups can easily accumulate into hundreds of dollars, providing a great supplementary boost to your primary, automated savings transfers.