Financial freedom is frequently portrayed as an exclusive club reserved for high-income earners, lucky lottery winners, or those who inherit massive fortunes. As a professional financial advisor, I often hear clients express the belief that building genuine wealth requires monumental sacrifices, a six-figure salary, or a perfectly timed market windfall. However, the truth of personal finance is far more accessible and profoundly more empowering. True financial security is rarely built on massive, one-time decisions; rather, it is constructed brick by brick through small, consistent habits that compound over time.

One of the most powerful illustrations of this principle is the concept of saving and investing a mere $10 every single day. At first glance, ten dollars feels entirely insignificant. It is the cost of a fast-food lunch, a couple of artisan coffees, or a fleeting impulse purchase online. Most of us let this amount slip through our fingers daily without a second thought. Yet, if you commit to redirecting that same $10 into your financial future every day for a decade, the mathematical and psychological outcomes are nothing short of extraordinary. This comprehensive guide will break down the exact mechanics of daily saving, explore the accelerative power of compound interest, provide actionable budgeting hacks to find hidden cash in your routine, and outline exactly where to invest your money for maximum growth. By mastering this micro-habit, you will discover that consistency matters infinitely more than your starting balance, and that the smallest daily actions can ultimately yield life-changing financial results.

The Simple Math Behind Saving $10 a Day

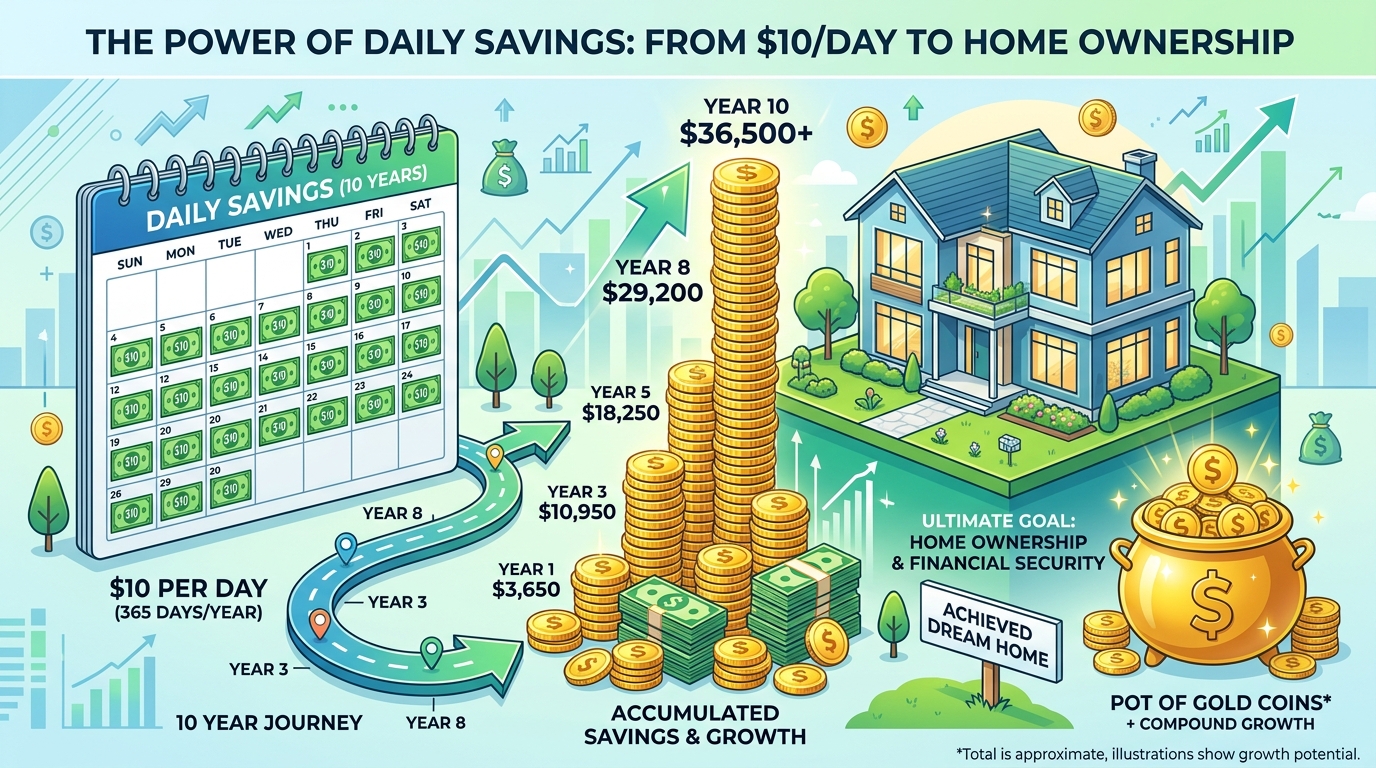

Before we introduce the magic of market returns, we must first establish the foundational mathematics of consistent saving. The raw numbers behind setting aside ten dollars daily are both sobering and encouraging. When you commit to this daily micro-habit, you are saving $70 every single week. Over the course of an average month, that translates to roughly $300 set aside. By the end of a single year, your principal savings will total $3,650.

Stretch that timeline out to a full decade, and you will have accumulated $36,500 in pure cash. It is vital to understand that this figure represents your principal alone—this is the result of simply putting money under a mattress or in a zero-interest checking account without touching investments, interest, or any external growth whatsoever. For the vast majority of households, having $36,500 in liquid cash is a profoundly life-changing amount of money. It is more than enough to fund a substantial down payment on a house, serve as the seed capital to launch a small business, pay for an advanced professional degree, or create an impenetrable emergency cushion that prevents you from ever falling into high-interest credit card debt during a crisis. Yet, this formidable financial fortress is nothing more than the sum of a small, entirely manageable daily action.

The Magic of Compound Interest: Accelerating Your Growth

While saving raw cash is a fantastic defensive financial strategy, the true wealth-building potential of the $10 a day habit is unlocked when you transition from a saver to an investor. This is where compound interest enters the equation. Often referred to as the eighth wonder of the world, compound interest is the process where your money earns interest, and then that interest earns interest, creating a snowball effect of exponential growth over time.

Imagine that instead of stashing your daily savings in a jar, you invest it in a diversified portfolio, such as a broad-market index fund or a retirement account. Historically, the stock market has averaged an annual return of roughly 7% to 10% over long periods, adjusting for inflation and market volatility. If you invest your $10 a day and achieve a conservative 7% annualized return, your $36,500 principal contribution will grow to approximately $52,000 over ten years. If the market performs closer to its historical average of 10%, your total balance could climb past $63,000.

That extra $15,500 to $26,500 did not come from working longer hours, taking on extra shifts, or depriving yourself of basic needs. It was generated entirely by the silent, relentless engine of compounding. This mathematical reality proves why starting early and staying consistent is the ultimate secret ingredient in wealth building. Time in the market allows your capital to multiply, meaning the earlier you begin this daily habit, the more powerful and disproportionate your financial rewards will become.

The Psychology of Wealth: Rewiring Your Money Mindset

As a financial advisor, I can confidently state that money management is 20% head knowledge and 80% behavior. Saving $10 a day is about far more than the raw numbers; it is a profound psychological exercise. One of the most significant barriers to personal finance success is decision fatigue. Every single day, consumers are bombarded with hundreds of micro-choices regarding whether to spend, save, or invest. This constant friction drains willpower and often leads to poor financial choices by the end of the day.

By creating a simple, automatic habit of setting aside $10 daily, you entirely remove the stress of decision-making from your financial life. You no longer have to debate whether you can afford to save; the decision has already been made for you. Over time, this automation fundamentally rewires your brain. Instead of viewing a $10 bill as disposable spending money meant for immediate gratification, you begin to subconsciously recognize it as a vital investment in your future self.

This paradigm shift in perspective inevitably ripples into other areas of your financial life. As you become more protective of your daily savings, you naturally become more intentional with your overall spending. You become less prone to emotional or impulse purchases, more mindful of lifestyle creep, and significantly more motivated to plan for long-term financial goals. You transition from a passive consumer to an active wealth builder, and that identity shift is often more valuable than the money itself.

Practical Budgeting Hacks: How to Find $10 a Day

A common objection to daily saving is the belief that there is simply no extra money in the budget. However, finding $10 a day is rarely about earning more; it is about plugging the “latte factor” leaks in your current spending. Almost anyone can redirect $10 from their daily routine without feeling deprived by employing a few strategic budgeting hacks.

First, audit your daily food and beverage spending. Brewing high-quality coffee at home instead of visiting a drive-through cafe can easily save $5 to $7 before you even leave your kitchen. Packing a lunch for work instead of ordering delivery with hidden fees and tips can save $15 or more daily. Second, conduct a ruthless subscription audit. Cancel streaming services, app subscriptions, or gym memberships that you rarely use, and redirect that monthly cost into a daily savings equivalent.

Third, implement the 24-hour rule for online shopping. When you feel the urge to make an impulse purchase online, force yourself to wait 24 hours. In the vast majority of cases, the emotional desire to buy the item will fade, and the money remains safely in your pocket. Finally, look for passive savings, such as negotiating your car insurance, switching to a cheaper mobile phone plan, or using cash-back apps for groceries. By stacking these small optimizations, finding $10 a day becomes an effortless byproduct of a more intentional lifestyle.

Where to Put Your Daily Savings: Beginner Investing Guide

Once you have successfully carved out $10 a day from your budget, the next critical step is determining where to deploy that capital for maximum efficiency. Leaving your daily savings in a standard brick-and-mortar checking account is a mistake, as inflation will silently erode your purchasing power over the decade. Instead, you must put your money to work in vehicles designed for growth.

For short-term goals or your foundational emergency fund, utilize a High-Yield Savings Account (HYSA). These accounts, typically offered by online banks, pay significantly higher interest rates than traditional banks, ensuring your cash is liquid, safe, and actively fighting inflation.

For long-term wealth building (the 10-year horizon and beyond), you should transition to the stock market via broad-market Index Funds or Exchange Traded Funds (ETFs), such as those tracking the S&P 500. This strategy provides instant diversification across hundreds of the largest companies, minimizing single-stock risk while capturing the overall growth of the economy. Furthermore, consider utilizing tax-advantaged accounts like a Roth IRA. By investing your daily savings into a Roth IRA, your money grows completely tax-free, and you can withdraw it tax-free in retirement, supercharging the compound interest effect. Investing a fixed amount daily or weekly is known as Dollar-Cost Averaging, a strategy that smooths out market volatility and removes the stress of trying to “time the market.”

Scaling Up: From $10 to Financial Independence

The true magic of the $10 a day strategy lies in its accessibility and scalability. Because the initial barrier to entry is so low, it is incredibly easy to build the habit. However, as your income grows through career advancements, side hustles, or raises, your savings rate should scale proportionally to avoid lifestyle creep.

Once the $10 a day habit feels entirely automatic and effortless, challenge yourself to increase the contribution to $15 or $20 a day. The mathematical impact of this slight increase is staggering. At $20 a day, you are saving $7,300 a year. Over a decade, your principal reaches $73,000. When you apply the same historical compound interest rates of 7% to 10%, that balance can easily surpass $100,000 to $125,000.

This scaling mechanism is the foundational engine behind the FIRE (Financial Independence, Retire Early) movement. The important takeaway is not the exact dollar amount you start with, but the unbreakable consistency of the habit. By proving to yourself that you can consistently save $10, you build the financial discipline required to eventually save $50 or $100 a day, rapidly accelerating your timeline to complete financial independence.

The Hidden Cost of Doing Nothing

When evaluating financial strategies, it is equally important to consider the alternative. What happens if you choose not to save that $10 a day? Where does that money actually go? For the majority of consumers, those daily micro-funds simply vanish into the ether of forgettable, low-value purchases. A premium takeout meal here, an upgraded streaming subscription there, or another fleeting online impulse buy.

Each of these transactions provides a quick, transient hit of dopamine and satisfaction, but absolutely none of them create lasting value or contribute to your net worth. This phenomenon is known in finance as opportunity cost—the loss of potential gain from other alternatives when one alternative is chosen. Ten years down the line, you will inevitably look back and realize that the stark difference between achieving financial stability and remaining in a cycle of financial struggle was not dictated by your salary, but by a series of tiny, seemingly insignificant daily decisions. Choosing inaction is still a choice, and it is a choice that actively works against your future financial security.

Real-Life Milestones: What Your Wealth Can Do For You

It is easy to get lost in the abstract mathematics of compound interest, but it is crucial to visualize what a portfolio valued at $60,000 or more can actually do for your life. Money, at its core, is simply a tool that provides options. Financial stress almost always stems from a lack of options and flexibility. When you accumulate resources, you purchase freedom.

A fully funded account of this size can serve as a robust emergency fund, covering six to twelve months of living expenses and allowing you to weather job losses or medical emergencies without panic. It can serve as the 10% to 20% down payment required to purchase your first home, transitioning you from a renter to a real estate owner. It can act as the seed capital to leave your corporate job and launch a passion-driven small business. Perhaps most importantly, it creates a “Walk Away” fund—the financial security required to leave a toxic work environment or an unhealthy relationship. The beauty of this daily habit is that the possibilities are entirely open-ended, granting you the confidence and security to design life on your own terms.

Building Unbreakable Financial Habits

As you embark on this journey, it is natural to worry about missing a day, facing an unexpected expense, or falling off track. However, in the realm of personal finance, consistency matters infinitely more than perfection. If you miss a day or two of saving, it will not derail your decade-long progress, provided you simply return to the habit immediately.

The key to long-term success is removing human error and willpower from the equation entirely by leveraging automation. Most modern brokerages and banking apps allow you to set up recurring daily or weekly transfers. By scheduling an automatic transfer of $70 every Sunday evening, you ensure the money is invested before you even have the opportunity to spend it. When your wealth building is automated, you no longer have to rely on motivation; the system does the heavy lifting for you while you focus on your career, family, and personal growth.

Conclusion

The real lesson of saving and investing a small amount daily is not just about the final dollar amount sitting in your brokerage account. It is about the profound internal transformation that takes place over the decade. You evolve from someone who spends unconsciously to someone who saves with deep purpose. You build resilience against economic emergencies, develop profound patience, and cultivate a quiet confidence that comes from knowing you are in control of your destiny. Building wealth does not require extraordinary circumstances, lottery tickets, or genius-level intellect; it simply requires ordinary, positive actions executed consistently over time. The next ten years are going to pass anyway. The only question is whether you will arrive at the finish line with nothing to show for it, or with a fortress of wealth built one small step at a time.

Frequently Asked Questions (FAQ)

1. Can I really build significant wealth saving just $10 a day?

Yes, absolutely. While $10 a day may seem small, the power of consistency combined with compound interest transforms it into a substantial sum. Over ten years, $10 a day is $36,500 in principal. When invested in the stock market with historical average returns, that balance can easily grow to over $60,000. Furthermore, this habit builds the financial discipline necessary to scale your contributions as your income rises, eventually leading to significant, life-changing wealth.

2. Is it better to save and invest daily, weekly, or monthly?

Mathematically, investing your money as soon as you receive it (daily) is slightly more advantageous because your capital enters the market sooner, giving it more time to compound. However, from a behavioral standpoint, the “best” frequency is the one you can automate and stick to consistently. If setting up daily transfers is cumbersome, automating a $70 weekly or $300 monthly transfer will yield nearly identical long-term results while being easier to manage.

3. What if the stock market crashes while I am investing my daily $10?

Market volatility is a normal part of long-term investing. When you invest a fixed amount regularly, you are utilizing a strategy called Dollar-Cost Averaging. During a market crash, your $10 will actually buy more shares of your index funds because the prices are lower. When the market inevitably recovers, those shares purchased at a discount will generate massive returns. Therefore, consistent daily investors should view market dips as buying opportunities, not reasons to panic.

4. Should I pay off high-interest debt before starting the $10 a day habit?

Generally, yes. High-interest debt, such as credit card balances charging 20% or more, will outpace the historical returns of the stock market (7% to 10%). From a purely mathematical standpoint, paying off a 20% interest credit card is equivalent to earning a guaranteed, tax-free 20% return on your money. However, some financial advisors recommend saving a small “starter” emergency fund of $1,000 to $2,000 first, to prevent you from relying on credit cards when unexpected minor expenses arise.

5. How do I automate my daily savings and investments?

Most modern financial institutions make automation incredibly simple. First, open a dedicated High-Yield Savings Account or a brokerage account (like a Roth IRA). Next, link it to your primary checking account. Within the app or website settings, look for the “Recurring Transfers” or “Automatic Investments” feature. You can set the system to pull $10 every day, or $70 every week, directly into your chosen investment fund. Once set up, monitor it occasionally, but let the system run on autopilot.