Ever look at your bank notification on payday and wonder where all your money went? You work hard, put in the hours, and expect a certain number to hit your account. Yet, when payday finally arrives, the final amount is often noticeably smaller than you imagined. This common experience leaves many professionals feeling confused, frustrated, and entirely disconnected from their own earnings.

If you do not know exactly what is being taken out of your check and why, it can easily feel like your employer or the government is arbitrarily cutting into your hard-earned income. But the truth is far less sinister. Your paycheck is simply a detailed mathematical breakdown of your compensation, divided into distinct categories: gross pay, mandatory taxes, voluntary benefits, and finally, your net pay.

Once you understand the anatomy of your paystub, you transform from a passive recipient of a paycheck into an active manager of your personal finances. You will never feel surprised by your take-home pay again. Instead of viewing your paystub as a confusing jargon-filled receipt, you will learn to read it as a powerful financial roadmap. This comprehensive guide will break down every single line item on your paycheck step by step, translating complex payroll terminology into plain, actionable language. By the end of this guide, you will know exactly where every dollar is going and how to optimize your earnings for your long-term financial goals.

10. Start with the Foundation: Understanding Gross Pay

The very first number you should look at on your paystub is your gross pay. This is the foundational starting point of your compensation. Gross pay represents the total amount of money you earn before absolutely anything is taken out. It is the raw value of your labor.

How this number is calculated depends entirely on your employment structure. If you are an hourly employee, your gross pay for that specific period is simply your hourly wage multiplied by the exact number of hours you worked. If you worked overtime, those hours will be calculated at your premium overtime rate (typically time-and-a-half) and added to the total. For example, if you make $25 an hour and worked a standard 40-hour week, your gross pay is $1,000.

If you are a salaried employee, the calculation is slightly different but equally straightforward. Your gross pay is your agreed-upon annual salary divided by the total number of pay periods in the year. If you are paid bi-weekly, your annual salary is divided by 26. If you are paid semi-monthly, it is divided by 24. Gross pay is a critical number to know because it is the baseline used to calculate your tax withholdings, your retirement contribution limits, and your eligibility for certain bonuses or benefits. It shows the total, uncompromised value of your professional work.

9. Understand Federal Income Tax Withholding

One of the most significant reasons your paycheck shrinks from gross to net is federal income tax. This is the money the federal government collects from you throughout the year to fund national programs, defense, and infrastructure. Rather than requiring you to pay this massive lump sum at the end of the year, the government uses a “pay-as-you-go” system, requiring your employer to withhold a portion of every paycheck and send it directly to the IRS on your behalf.

The exact amount withheld depends on several dynamic factors: your total income level, your tax filing status (such as single, married filing jointly, or head of household), and the specific information you provided on your W-4 form when you were hired. Employers use IRS tax bracket tables to calculate this withholding. It is important to remember that the US uses a progressive tax system, meaning different portions of your income are taxed at different rates.

If you withhold too much throughout the year, you will receive a tax refund in the spring. While a refund feels like a bonus, it actually means you gave the government an interest-free loan of your own money. Conversely, if you withhold too little, you will owe a lump sum when you file your taxes. Reviewing and updating your W-4 form after major life events—like getting married, having a child, or buying a house—ensures your withholding remains perfectly calibrated to your actual tax liability.

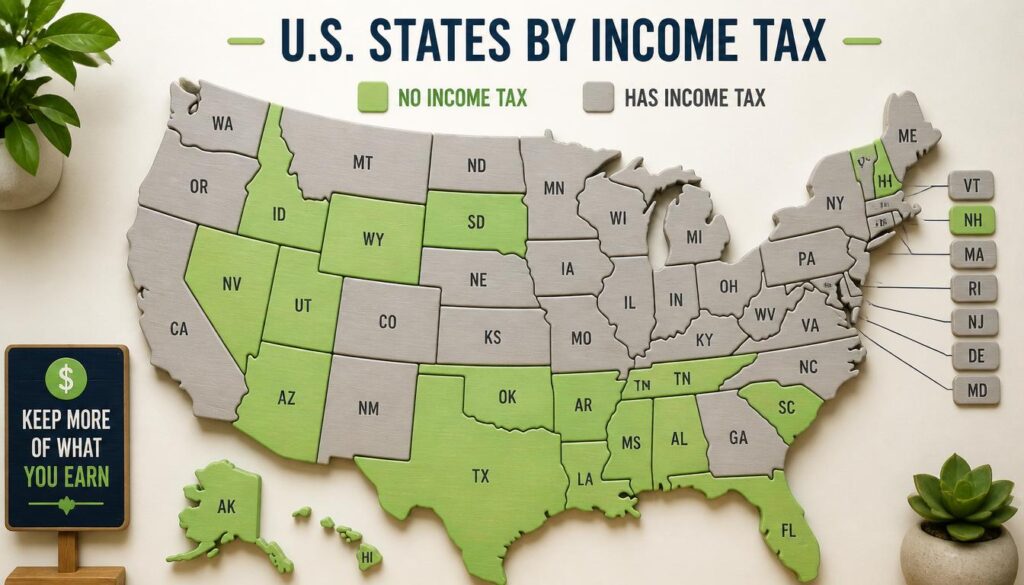

8. Look at State and Local Taxes

Depending on where you live and work, you will likely see another deduction for state income tax. These taxes function similarly to federal taxes but are collected by your state government to fund local programs such as public schools, state highways, and regional healthcare initiatives.

The impact of state taxes varies wildly depending on your geography. If you live in a high-tax state like California, New York, or New Jersey, this deduction will be a significant chunk of your paycheck. On the other hand, if you reside in a state with no income tax, such as Texas, Florida, Nevada, or Washington, this line item will be completely absent from your paystub, leaving you with more take-home pay.

Furthermore, if you live in certain major metropolitan areas, you might also see a local or city tax deducted. For instance, residents of New York City or certain cities in Ohio and Pennsylvania are subject to municipal income taxes. Understanding your state and local tax burden is crucial, especially if you are considering a job offer in a different state or transitioning to a remote work arrangement that changes your tax residency.

7. Understand Social Security Contributions

Scrolling down your paystub, you will encounter a line item labeled “Social Security,” “Soc Sec,” or “OASDI” (Old-Age, Survivors, and Disability Insurance). This is the first half of your FICA (Federal Insurance Contributions Act) taxes. Social Security is a vital federal program designed to provide a safety net of income for retirees, individuals with severe disabilities, and the surviving dependents of workers who have passed away.

Under current law, the employee contribution for Social Security is a flat 6.2% of your gross wages, but only up to a specific annual wage base limit. Once your earnings exceed that cap for the year, Social Security taxes are no longer withheld from your subsequent paychecks.

What makes this deduction particularly special is the employer match. For every 6.2% that is taken from your paycheck, your employer is legally required to contribute an identical 6.2% out of their own pocket directly to the Social Security administration. While seeing 6.2% leave your paycheck might sting in the short term, it is a mandatory, guaranteed investment in your future financial security, ensuring you have a baseline of income when you eventually retire.

6. Understand Medicare Contributions

Right next to Social Security on your paystub, you will see the deduction for Medicare. This is the second half of your FICA taxes. Medicare is the federal health insurance program primarily designated for Americans aged 65 and older, as well as certain younger individuals with specific disabilities or end-stage renal disease.

The current Medicare tax rate is a flat 1.45% of your gross wages. Unlike Social Security, there is no wage base limit for Medicare; you pay this tax on every single dollar you earn, no matter how high your income goes. Just like Social Security, your employer matches this contribution dollar-for-dollar with their own 1.45% payment.

It is also worth noting that high-income earners are subject to an Additional Medicare Tax. If your wages exceed a certain threshold (which varies based on your filing status), an extra 0.9% will be withheld from your paycheck specifically for Medicare. While these funds are not accessible to you today, they are actively funding the healthcare infrastructure that will support you and millions of others in your senior years.

5. Take Note of Pre-Tax Benefits

Not all deductions are mandatory taxes; many are voluntary benefits that you have elected to participate in. A major category of these is pre-tax benefits, which commonly include premiums for health insurance, dental insurance, vision insurance, and life insurance.

The magic of pre-tax benefits lies in the order of operations on your paystub. These deductions are taken out of your gross pay before federal and state income taxes are calculated. This mechanically lowers your overall taxable income. For example, if your gross pay is $4,000 for the month and you pay $300 for your portion of the employer’s health insurance plan, the government only calculates your income tax based on $3,700.

By utilizing pre-tax benefits, you effectively lower your overall tax burden while still securing vital protection for your health and your family’s well-being. It is a highly efficient way to pay for necessary insurance, as you are essentially getting a discount equal to your marginal tax rate on every dollar you spend on those premiums.

4. Look for Retirement Contributions

If your employer offers a retirement plan, such as a 401(k), 403(b), or 457 plan, and you have chosen to participate, you will see a deduction for your retirement contributions. This is arguably the most important line item on your paystub for your long-term wealth generation.

When you contribute to a traditional pre-tax retirement account, the money is deducted before taxes are calculated, similar to health insurance, giving you an immediate tax break for the year. If you contribute to a Roth option (if available), the money is deducted after taxes, but your money grows tax-free and can be withdrawn tax-free in retirement.

The most critical aspect of this deduction is the employer match. Many companies offer to match your contributions up to a certain percentage of your salary. For instance, if you contribute 5% of your paycheck, your employer might also contribute 5%. This match is essentially a 100% immediate, guaranteed return on your investment. It is free money that dramatically accelerates your compound interest over time. Maximizing this deduction to at least the level of your employer’s match should be a top priority in your financial planning.

3. Don’t Forget Other Deductions

Depending on your unique personal circumstances, union membership, or financial obligations, your paystub may feature a variety of other miscellaneous deductions. It is vital to understand these so they do not catch you off guard.

You might see deductions for union dues if you are part of a labor organization. You may also see wage garnishments, which are court-ordered deductions for unpaid child support, alimony, or defaulted student loans. While garnishments are mandatory, you have the right to understand the legal limits of how much of your paycheck can be garnished.

Additionally, you might see contributions to a Health Savings Account (HSA) or a Flexible Spending Account (FSA). If you are enrolled in a High Deductible Health Plan (HDHP), an HSA is an incredibly powerful tool. Contributions are pre-tax, the money grows tax-free if invested, and withdrawals for qualified medical expenses are also tax-free—a rare “triple tax advantage.” An FSA operates similarly for pre-tax medical expenses, though it often comes with a “use it or lose it” rule at the end of the plan year. Always review these deductions to ensure the amounts align with your elections.

2. Calculate Your Net Pay (Take-Home Pay)

After gross pay has been reduced by federal taxes, state taxes, FICA, pre-tax benefits, retirement contributions, and any other miscellaneous deductions, you arrive at the final number: your net pay. This is also commonly referred to as your take-home pay. This is the exact amount of money that is directly deposited into your checking account.

Net pay is the single most important number on your paystub when it comes to your daily life. It represents your actual purchasing power. A common and dangerous financial mistake is building a monthly budget based on your gross salary. When you do this, you inevitably overestimate your available funds, leading to shortfalls, credit card debt, and financial stress.

When planning your budget, you must strictly use your net pay. A popular and effective framework is the 50/30/20 rule: allocate 50% of your net pay to needs (housing, groceries, utilities), 30% to wants (dining out, entertainment, hobbies), and 20% to savings and debt repayment. By anchoring your financial life to your net pay, you maintain a realistic, stress-free grasp on your true financial reality.

1. Review Your Paystub Regularly

The final and most crucial step in mastering your paycheck is making the review of your paystub a consistent habit. Do not just glance at the net deposit amount and delete the email or throw away the paper. Take five minutes every single pay period to scan the entire document.

Why is this so important? First, employers and payroll departments are human; mistakes happen. An incorrect hourly entry, a missed overtime calculation, or a duplicated deduction can easily slip through. Catching these errors early ensures you are paid accurately and makes it much easier for payroll to correct the mistake in the next cycle.

Second, your life changes, and your paystub should reflect those changes. If you recently got married, had a baby, or paid off a massive student loan, your tax withholding and deduction needs have changed. Reviewing your paystub regularly prompts you to update your W-4 or adjust your benefit elections. This habit transforms you from a passive employee into an proactive financial advocate for yourself, ensuring your money is working exactly the way you want it to.

Conclusion

Your paycheck is far more than just a notification of funds hitting your bank account; it is a comprehensive financial roadmap. It details exactly how your hard work is divided between government taxes, vital social safety nets, personal benefits, and your future retirement. By taking the time to understand every component—from gross pay and FICA taxes to pre-tax benefits and your final net pay—you eliminate the confusion and anxiety that often surrounds payday.

Instead of wondering where your money went, you now possess the knowledge to track every single dollar. This financial literacy is the foundational first step toward taking absolute control of your economic life. When you understand your income, you can budget smarter, optimize your taxes, maximize your employer benefits, and make confident, strategic decisions that align with your long-term wealth-building goals. Take control of your paystub today, and watch your financial confidence grow.

Frequently Asked Questions (FAQ)

1. What is the exact difference between gross pay and net pay?

Gross pay is the total amount of money you earn before any deductions, taxes, or benefits are taken out. It is your raw income. Net pay, often called take-home pay, is the final amount left over after all mandatory taxes (federal, state, FICA) and voluntary deductions (health insurance, retirement contributions) have been subtracted. Net pay is the actual money that gets deposited into your bank account and is the number you should use to build your monthly budget.

2. Why did my paycheck shrink even though my salary or hourly rate didn’t change?

There are several reasons your take-home pay might decrease without a change in your base salary. The most common reason is a change in your tax withholding, perhaps due to an updated W-4 form or a change in your tax bracket as your year-to-date income pushes you into a higher bracket. Other reasons include the expiration of a pre-tax benefit open enrollment period, an increase in your health insurance premiums, or the cessation of a temporary tax holiday. Always compare your year-to-date totals and deductions to pinpoint the exact change.

3. How can I change the amount of federal taxes withheld from my paycheck?

To change your federal tax withholding, you need to submit a new Form W-4 to your employer’s human resources or payroll department. The modern W-4 form allows you to adjust your withholding by claiming dependents, entering additional income from other jobs, or requesting a specific additional dollar amount to be withheld from each check. It is highly recommended to use the IRS Tax Withholding Estimator tool online to calculate the exact adjustments you need to avoid owing a large bill or giving the government an interest-free loan.

4. Are pre-tax deductions better than post-tax deductions?

Neither is universally “better”; it depends on your current financial situation and goals. Pre-tax deductions (like traditional 401(k) contributions or health insurance premiums) lower your taxable income today, giving you an immediate tax break and increasing your current take-home pay slightly. Post-tax (Roth) deductions do not lower your current taxable income, but they allow your money to grow tax-free and be withdrawn tax-free in retirement. A common strategy is to use pre-tax deductions to lower your current tax burden while using Roth options for long-term tax diversification.

5. What should I do if I spot an error on my paystub?

If you notice an error, such as incorrect hours worked, missing overtime, or an unauthorized deduction, act immediately. Do not wait. Contact your payroll department or human resources representative in writing (via email) so there is a documented record of your claim. Provide your paystub, highlight the error, and provide any supporting documentation, such as your own time-tracking records or approval emails. Payroll departments are generally very responsive to correcting mistakes, especially if caught within the same pay period or shortly after.