Planning a vacation is inherently exciting, but the financial reality of funding that getaway can quickly transform excitement into anxiety. For many individuals and families, saving for travel feels like a daunting task, especially when navigating the constraints of a tight monthly budget. The prevailing myth is that luxurious getaways or even modest weekend escapes are reserved only for the financially elite. However, the truth is that with deliberate strategy, disciplined financial habits, and a clear roadmap, you can systematically set aside money for your dream getaway without breaking the bank or accumulating high-interest debt.

Whether you are aiming for a serene weekend escape to a nearby cabin, a backpacking adventure through diverse landscapes, or a meticulously planned international expedition, the foundational principles of travel savings remain the same. The key lies in creating a realistic, data-driven savings plan, ruthlessly eliminating unnecessary expenses, and discovering creative, sustainable ways to grow your dedicated vacation fund. This comprehensive guide will explore practical, actionable tips and proven financial strategies to help you save for your vacation without stressing over your everyday finances. By treating your travel fund with the same seriousness as a retirement account or an emergency fund, you can turn your wanderlust into a tangible, achievable reality.

1. Define Your Travel Dreams and Budgetary Reality

Before you can save effectively, you must first define exactly what you are saving for. Vague goals like “I want to travel more” rarely yield results because they lack a specific financial target. This step is not merely about picking a destination on a map; it is about crafting a detailed, comprehensive travel vision that aligns with your financial reality.

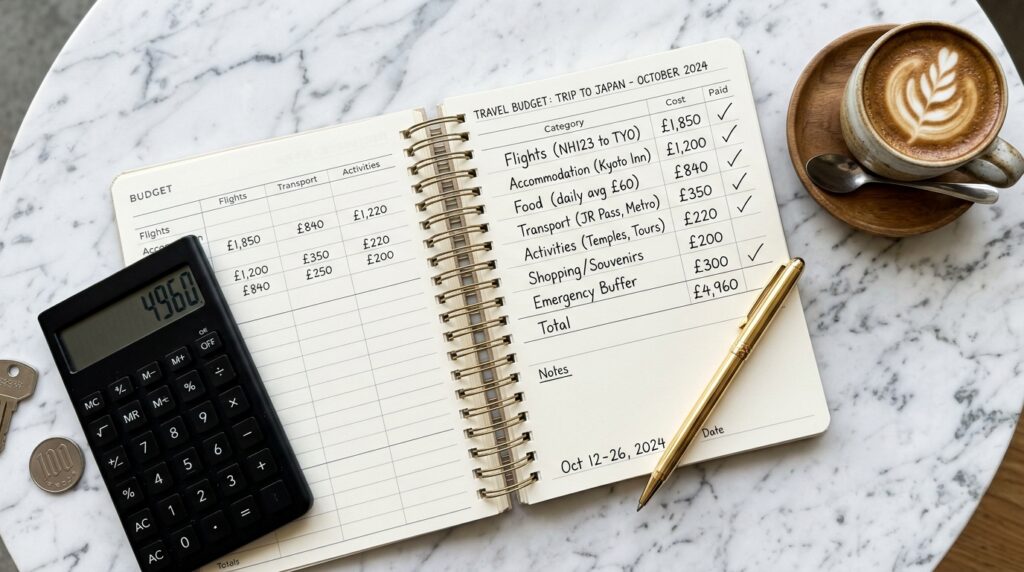

Do you dream of a luxurious, all-inclusive week at a resort, a rugged backpacking adventure through Southeast Asia, or a family-friendly road trip across the American Southwest? Each of these scenarios carries a vastly different price tag. Start by conducting thorough research to estimate the total costs for your desired trip. Break down the expenses into granular categories: round-trip flights, accommodation, daily food and dining, planned activities and tours, local transportation, travel insurance, and, crucially, a buffer of at least 15% for unexpected expenses like currency fluctuations or emergency medical needs.

This meticulous research forms the unshakeable foundation of your savings goal. You must be brutally realistic with yourself. If a two-week trip to Tokyo appears mathematically out of reach based on your current income and a one-year savings timeline, consider pivoting to a closer, more affordable alternative that offers a similar cultural richness, such as Montreal or Mexico City. Remember, the ultimate goal is to enjoy the travel experience without the looming shadow of financial stress. That peace of mind starts with setting a tangible, highly specific, and achievable savings target. Once you have the total estimated cost, break it down into a manageable monthly or bi-weekly savings goal to make the mountain feel like a series of climbable hills.

2. Automate Your Savings for Guaranteed Consistency

The single most effective, battle-tested strategy for saving money is to completely automate the process. Relying on willpower to manually transfer money at the end of the month is a flawed strategy, as it leaves room for human error, forgetfulness, and the ever-present temptation to spend money on immediate gratification before it has a chance to be saved. Automation removes the psychological friction of saving.

To implement this, set up an automatic, recurring transfer from your primary checking account to a dedicated high-yield savings account (HYSA) scheduled for every payday. The amount you transfer should perfectly align with the monthly savings goal you established in the previous step. For example, if your research dictates that you need to save $300 a month, configure your bank to automatically transfer $150 on the 1st and 15th of each month. This practice, known in personal finance as “paying yourself first,” ensures your travel fund is prioritized before discretionary spending can occur.

Choosing a high-yield savings account is crucial for this strategy. Unlike traditional brick-and-mortar bank savings accounts that offer negligible interest rates, an HYSA allows your money to grow on its own through compound interest. While the growth may seem modest in the short term, it actively combats inflation and ensures your purchasing power remains intact. Furthermore, the key to success is making this account deliberately difficult to access for everyday spending. By keeping it at a separate financial institution from your primary checking account and not linking it to a debit card, you create a powerful psychological barrier that prevents impulse withdrawals. Treat this account as a sacred vault; once the money is deposited, it is legally and mentally designated solely for your vacation.

3. Accelerate Your Fund with a Strategic Side Hustle

Sometimes, aggressive expense cutting alone is not enough to reach an ambitious vacation savings goal within your desired timeframe, or it may require a level of lifestyle sacrifice that is simply unsustainable. This is where a strategic side hustle becomes a true game-changer. By generating additional, dedicated income streams, you can dramatically accelerate your savings timeline without drastically altering your baseline lifestyle or dipping into your emergency fund.

Begin by taking an inventory of your existing skills, assets, and interests. Can you freelance as a graphic designer, copywriter, or web developer on platforms like Upwork or Fiverr? Do you have a flexible schedule that allows you to offer weekend dog walking, pet sitting, or house sitting services? Perhaps you possess strong organizational skills and can help local residents declutter and organize their homes for a fee. Other highly accessible options include driving for a rideshare company, delivering food, or selling gently used items you no longer need on digital marketplaces like eBay, Poshmark, or Facebook Marketplace.

The absolute golden rule of using a side hustle for travel savings is allocation. You must dedicate every single dollar earned from this secondary income stream directly to your vacation fund. Resist the powerful temptation to absorb this extra money into your general checking account to fund lifestyle creep, such as upgrading your daily coffee order or buying new clothes. By mentally and physically earmarking this income solely for travel, you create a direct, rewarding link between your extra effort and your dream destination, making the hustle feel purposeful rather than exhausting.

4. Cut Back on Daily Expenses Without Losing Your Mind

A critical, non-negotiable component of any successful savings plan is examining your current spending habits and ruthlessly identifying areas where you can cut back. You cannot manage what you do not measure. Start by tracking every single dollar you spend for at least 30 consecutive days. Utilize a dedicated budgeting app or a simple, customized spreadsheet to categorize your spending into buckets like groceries, dining out, entertainment, subscriptions, and retail shopping.

This auditing process is frequently eye-opening. It reveals the “hidden” small daily expenses that seem insignificant in isolation but compound into massive financial leaks over time. For instance, a $6 daily specialty coffee might not feel like a budget breaker, but it amounts to over $2,100 annually. Instead of completely eliminating these small luxuries, which can lead to budget burnout and rebellion, find cheaper, sustainable alternatives. Brew high-quality coffee at home, pack a nutritious lunch instead of eating at expensive restaurants, or temporarily cancel one of your redundant streaming subscriptions for a few months.

Beyond daily habits, conduct a thorough review of your recurring bills and annual subscriptions. Identify gym memberships you rarely use, magazine subscriptions you never read, or premium app features you do not need. Furthermore, take the initiative to call your internet, mobile phone, or cable provider. Customer retention departments are often authorized to offer promotional rates or waive fees simply because you asked. Negotiating these fixed costs can free up a significant chunk of your monthly budget to be redirected straight into your travel fund.

5. Master Smart Shopping and Strategic Spending

When it comes to purchasing items you truly need, there are still abundant opportunities to optimize your spending. The key is to transition from being a passive consumer to a strategic, savvy shopper. Before buying any non-essential item, institute a mandatory 24-hour cooling-off period. Ask yourself if the item is a genuine “need” or a fleeting “want.” This brief pause disrupts the emotional impulse to buy and often reveals that the item was not as necessary as it initially seemed, saving you money effortlessly.

When a purchase is unavoidable, actively hunt for deals and discounts. Utilize reputable coupon apps and browser extensions that automatically search for and apply promotional codes at checkout. Embrace the secondhand market for clothing, furniture, electronics, and other goods. Shopping at thrift stores or online resale platforms is not only exceptional for your wallet, but it also reduces your carbon footprint, aligning your financial goals with environmental consciousness.

Additionally, take strategic advantage of loyalty programs and credit card rewards. If you possess the financial discipline to use a credit card responsibly and pay off the statement balance in full every single month to avoid interest, you can earn substantial cash back or travel points. These rewards can be strategically redeemed to directly offset the cost of your vacation flights, hotel stays, or rental cars, effectively giving you a discount on your trip for money you were already planning to spend.

6. Make Big Sacrifices for Big Results

While trimming daily expenses is a vital foundational step, a significant or accelerated savings goal sometimes requires making bigger, more impactful, temporary sacrifices. This involves evaluating your broader financial timeline and strategically postponing major life events or large purchases to prioritize your travel goal.

Ask yourself critical questions: Are you planning to buy a new car this year? Could you hold off for another twelve months, maintaining your current reliable vehicle, and redirect that massive car payment or down payment toward your dream trip? Are you contemplating a costly home renovation? Perhaps you can postpone that project until after your vacation, enjoying the memories first and funding the renovation later.

Even smaller, yet significant, lifestyle adjustments can make a massive dent in your savings goal. Consider forgoing an expensive weekend getaway with friends in favor of hosting a budget-friendly potluck or game night at your home. If you have a costly hobby, such as golfing, skiing, or frequent concert-going, you could temporarily reduce the frequency of these activities. The psychological key to enduring these sacrifices is framing them not as permanent deprivations, but as temporary, intentional trade-offs with a clear, exciting, and highly rewarding goal at the finish line. You are not losing out; you are investing in an experience.

7. Leverage Modern Financial Tools and Resources

In today’s digital age, you do not have to navigate your financial journey alone. There are countless sophisticated, user-friendly tools and resources available to help you save, track, and manage your money with precision. Taking full advantage of this technology can streamline your efforts and provide invaluable insights.

Utilize comprehensive budgeting applications like YNAB (You Need A Budget), EveryDollar, or Monarch Money to get a crystal-clear, real-time picture of your finances. These apps securely connect to your bank accounts and automatically categorize your spending, highlighting trends and instantly identifying areas where you are overspending.

Additionally, look into micro-investing or micro-saving apps like Acorns or Qapital. These innovative tools can be set to round up your everyday purchases to the nearest dollar and invest or save the spare change. While this should not be your primary savings strategy, it operates as a painless, “set-it-and-forget-it” method that can surprisingly add up over several months. Finally, if you have secured a specific travel rewards credit card, ensure you thoroughly understand how to maximize its unique rewards and point system. Some premium cards offer lucrative sign-up bonuses that, when met through normal spending, can cover a significant portion of a round-trip flight or several nights in a hotel.

8. Stay Motivated and Celebrate Your Milestones

Saving for a vacation can be a marathon, not a sprint, and it is entirely normal to experience dips in motivation along the way. To stay rigorously on track, it is essential to keep your travel dream visually and mentally front and center. Create a physical or digital vision board featuring high-quality pictures of your destination, the specific activities you want to experience, and the local cuisine you want to taste. Place a photo of your dream destination on your refrigerator, your office bulletin board, or as your phone’s lock screen. This constant visual reinforcement keeps your “why” alive.

Make it a habit to regularly check your dedicated savings account balance to visually witness your progress. Numbers on a screen provide tangible proof that your efforts are working. Crucially, you must celebrate small milestones to maintain momentum. When you reach 25% of your savings goal, treat yourself to a small, inexpensive reward, such as your favorite coffee or a movie night at home. When you hit the halfway point, perhaps you can have a celebratory, budget-friendly dinner with your saving partner or friends. These small, planned rewards reinforce the positive neurological feedback loop of saving and prevent budget burnout, ensuring you cross the finish line with enthusiasm rather than exhaustion.

Conclusion

Saving for a vacation on a tight budget is not about depriving yourself of joy; it is about intentionally redirecting your resources toward experiences that truly matter to you. By defining a clear, realistic budgetary target, automating your contributions to a high-yield savings account, and supplementing your income with a dedicated side hustle, you build an unbreakable financial foundation. Coupled with mindful daily spending, strategic shopping, and the occasional calculated sacrifice, your dream trip transitions from a distant fantasy to an inevitable reality. Leverage modern financial tools to keep yourself accountable, and never forget to celebrate the milestones along the way. With discipline, strategy, and a clear vision, you can pack your bags and embark on your adventure completely debt-free and financially secure.

Frequently Asked Questions (FAQ)

1. How much should I realistically save for a vacation on a tight budget?

The amount varies wildly based on your destination, travel style, and duration. However, a good rule of thumb is to estimate the total cost of flights, accommodation, food, activities, and a 15% emergency buffer, then divide that total by the number of months until your trip. For a modest domestic trip, this might be $50–$100 per month, while an international trip could require $200–$400 per month.

2. Is a high-yield savings account (HYSA) really necessary for my vacation fund?

Yes. While a traditional savings account might offer 0.01% APY, a high-yield savings account can offer significantly higher rates, allowing your money to combat inflation and grow passively. More importantly, keeping this account at a separate bank creates a psychological barrier, making it less tempting to dip into the funds for everyday expenses.

3. What are the best side hustles specifically for building a travel fund quickly?

The best side hustles are those that offer immediate or weekly payouts and align with your existing skills. Freelance writing, graphic design, virtual assistance, pet sitting, food delivery, and selling unused household items on digital marketplaces are highly effective because you can directly earmark 100% of this specific income stream to your travel account.

4. How can I use credit cards to save for a vacation without going into debt?

You can use travel rewards credit cards to earn points or cash back on your everyday, necessary spending (like groceries and gas). The absolute golden rule is to treat the credit card like a debit card: you must pay the statement balance in full every single month before the due date to avoid any interest charges. If you carry a balance, the interest will instantly negate any value from the rewards.

5. What should I do if I fall behind on my vacation savings goal?

Do not panic or abandon the plan. First, reassess your timeline. Can you push the trip back by a few months to reduce the monthly burden? Second, review your budget to identify any new areas to cut back, or temporarily increase your side hustle hours. Finally, if necessary, scale down the scope of the trip (e.g., choosing a cheaper destination or shortening the duration) to ensure you can still travel without financial stress.