Real estate has long been considered one of the most reliable and powerful paths to building long-term wealth. Unlike the stock market, which can be highly volatile, or traditional savings accounts, which often yield minimal returns that fail to outpace inflation, real estate offers a unique combination of steady monthly income, long-term property appreciation, and tangible ownership. However, for beginners, the world of property investment can feel incredibly overwhelming. Complex terminology, high entry costs, and the fear of making a costly mistake often keep aspiring investors on the sidelines.

Terms like rental property investing, house hacking, and Real Estate Investment Trusts (REITs) may seem intimidating at first glance. But with the right breakdown and a solid understanding of the fundamentals, these strategies are highly accessible, even for someone starting with limited capital. This comprehensive guide will demystify the real estate market, breaking down the core strategies, financing options, and mathematical principles you need to start investing in property the smart way.

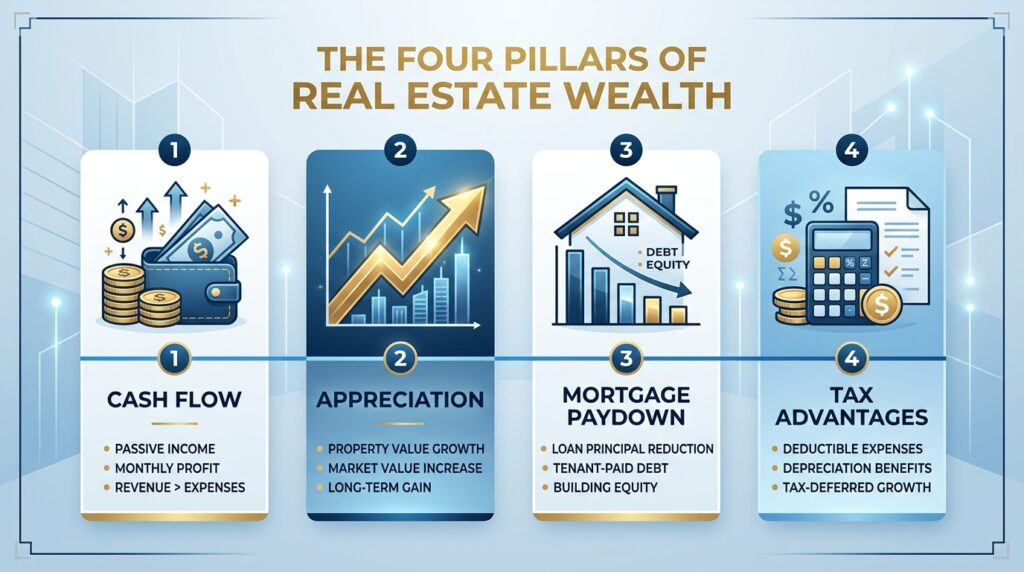

The Four Pillars of Real Estate Wealth Creation

Before diving into specific strategies, it is crucial to understand why real estate is such a powerful investment vehicle. Real estate is not just about buying a house and hoping it goes up in value; it is a multifaceted asset class that provides multiple concurrent streams of wealth creation.

1. Monthly Cash Flow: When you purchase a rental property and lease it to tenants, the rent collected ideally exceeds your monthly expenses (mortgage, taxes, insurance, and maintenance). This surplus is your monthly cash flow, providing a steady stream of passive income that can supplement your salary or fund your retirement.

2. Property Appreciation: Historically, real estate values tend to increase over time. While short-term fluctuations occur due to market conditions, long-term appreciation builds your net worth. As the property value rises, your equity grows, providing a significant return on investment when you eventually sell or refinance.

3. Mortgage Paydown (Amortization): This is the hidden wealth builder. When you have a rental property, your tenant is essentially paying your mortgage. With every monthly payment, a portion goes toward the principal balance. Over time, your loan balance decreases, and your equity increases, forced savings funded by someone else.

4. Tax Advantages: The tax code heavily favors real estate investors. You can deduct expenses such as property taxes, insurance, maintenance, and mortgage interest. More importantly, you can claim depreciation—a non-cash expense that allows you to deduct the cost of the building over time against your rental income, significantly lowering your taxable income.

Furthermore, real estate allows for leverage. Unlike stocks, where you typically need 100% of the capital to buy $100,000 worth of shares, a bank will lend you most of the cost of a property while you only put down a fraction (e.g., 20%). If you put $20,000 down on a $100,000 property and it appreciates by 5% ($5,000), your return on your actual cash invested is 25%, not 5%. This magnification of returns is the true superpower of real estate.

Defining Your Real Estate Investment Goals

Not all real estate strategies are created equal, and what works for one investor may be a terrible fit for another. Before spending a dime, you must define your primary objective. Are you seeking immediate monthly cash flow to replace your W-2 income, or are you more interested in long-term wealth building through appreciation and equity growth?

Your goals will dictate your strategy. If you want high monthly cash flow, you might look for multi-family properties in emerging, working-class neighborhoods where cap rates are higher. If you prefer long-term appreciation with minimal day-to-day hassle, you might target single-family homes in established, high-demand school districts.

Additionally, you must assess your desired level of involvement. Do you want an active business where you manage tenants, coordinate repairs, and handle late-night emergency calls? Or are you looking for a completely passive investment where you simply collect a dividend check? Answering these questions will narrow down your options and prevent you from pursuing a strategy that leads to burnout.

Top Real Estate Strategies for Beginners

Once your goals are set, you can choose the vehicle that best aligns with your vision. Here are the three most accessible entry points for new investors.

1. Traditional Rental Property Investing

Buying a dedicated rental property is the most classic entry point into real estate. This involves purchasing a single-family home, a duplex, or a small apartment building specifically to lease it out to tenants. The math is straightforward: you collect rent, pay the expenses, and keep the difference.

For beginners, single-family homes are often the most attractive because they are easier to finance, easier to sell later, and attract long-term tenants who treat the property like their own. However, they only provide one door of income. If the tenant leaves, your cash flow drops to zero until you find a replacement. Small multi-family properties (duplexes to four-plexes) offer a great compromise, providing multiple income streams while still qualifying for favorable residential mortgage rates.

2. House Hacking: Living and Investing Simultaneously

If buying a dedicated rental property feels financially intimidating, house hacking is the ultimate beginner-friendly strategy. House hacking involves purchasing a multi-unit property (like a duplex or triplex), living in one unit, and renting out the others. Alternatively, you can buy a single-family home with extra bedrooms and rent out individual rooms.

The magic of house hacking is that the rental income from your tenants or roommates helps cover your mortgage, property taxes, and insurance. In many cases, this reduces your personal living expenses to zero, or even generates a small profit. This strategy is incredibly powerful because it allows you to qualify for a primary residence mortgage (which requires a much lower down payment, often just 3% to 5%) while gaining invaluable experience as a landlord. You learn how to manage tenants and maintain a property, but because you live on-site, handling issues is much more convenient.

3. REITs: The Hands-Off Approach for Passive Investors

Not everyone wants the responsibility of managing toilets, dealing with tenant disputes, or worrying about roof repairs. If you want exposure to real estate without becoming a landlord, Real Estate Investment Trusts (REITs) are the perfect solution. (Note: Often misheard as “riots” by auto-captions, REITs are a cornerstone of passive investing).

A REIT is a company that owns, operates, or finances income-producing real estate. By investing in a REIT, you are buying shares in a massive portfolio of properties, which could range from apartment complexes and shopping centers to data centers and hospitals. REITs trade on major stock exchanges, meaning you can buy and sell them as easily as shares of Apple or Microsoft. By law, REITs must pay out at least 90% of their taxable income to shareholders as dividends, making them an excellent vehicle for generating high, consistent passive income without ever dealing with a physical property.

Financing Your First Real Estate Investment

Understanding how to finance your purchase is just as critical as finding the right property. Real estate is unique because you can use Other People’s Money (OPM) to control a high-value asset.

Traditional Conventional Loans: These require good credit and typically a 20% to 25% down payment for an investment property. They offer competitive interest rates but require significant upfront capital.

FHA Loans: Insured by the Federal Housing Administration, these loans are a house hacker’s best friend. They allow you to buy a property with as little as 3.5% down, provided you live in the property for at least a year. This is the primary financing tool for the house hacking strategy mentioned earlier.

VA Loans: Available to eligible veterans, active-duty service members, and surviving spouses, VA loans offer the incredible benefit of zero down payment and no private mortgage insurance (PMI).

Creative Financing: As you gain experience, you might explore partnerships (pooling money with a partner who has capital while you provide the sweat equity), private money lenders (borrowing from individuals in your network), or seller financing (where the seller acts as the bank).

However, leverage is a double-edged sword. While it magnifies your returns when a property performs well, it also magnifies your losses if the property sits vacant or requires massive repairs. Always ensure your deal cash-flows positively, even under conservative assumptions, so you are never forced to pay out of pocket just to keep the property afloat.

Running the Numbers: The Math Behind the Deal

The single biggest mistake beginners make is letting their emotions guide their purchasing decisions. Falling in love with a beautiful kitchen or a gorgeous backyard will not pay the mortgage. Successful investors are strictly analytical; they let the numbers dictate their decisions.

When evaluating a property, you must calculate the Net Operating Income (NOI) and your Cash-on-Cash return. To do this, you must account for every single expense, not just the mortgage.

The Hidden Expenses:

- Property Taxes and Insurance: These can rise significantly after you purchase the property.

- Vacancy Rate: Properties will not be rented 100% of the time. Always budget for a 5% to 10% vacancy rate to cover months when the unit is empty.

- Capital Expenditures (CapEx): Roofs leak, HVAC systems die, and water heaters break. You must set aside a portion of the rent (typically 5% to 10%) every month into a reserve fund for these inevitable large replacements.

- Property Management: If you do not want to manage the property yourself, a property manager will typically charge 8% to 10% of the monthly rent.

The 1% Rule: A popular quick-filter guideline is the 1% rule, which suggests that the monthly rent should equal at least 1% of the total purchase price. For a $200,000 property, it should rent for at least $2,000 a month. While this rule is harder to achieve in today’s high-priced markets, the underlying principle remains vital: the rent must be high enough to comfortably cover all expenses and still leave a profit. Never buy a property simply hoping it will appreciate enough to cover a negative monthly cash flow.

Managing Risks and Building Your Dream Team

Like any investment, real estate carries inherent risks. Tenants might stop paying rent, requiring a lengthy and expensive eviction process. Unexpected repairs can wipe out your cash flow for the year. Economic downturns can temporarily depress property values, and rising interest rates can make refinancing expensive.

The key to managing these risks is preparation. Always maintain a robust cash reserve fund—ideally three to six months of mortgage payments and operating expenses—so you are never caught off guard. Carry adequate landlord insurance to protect against liability and property damage. Furthermore, diversify your approach; perhaps you own one physical rental property but also invest in REITs to balance your portfolio.

Equally important is building a strong support network. Real estate is a team sport. You should not attempt to do everything yourself. Start building your “dream team” early:

- A knowledgeable Real Estate Agent: Someone who understands investment properties, not just residential homebuyers.

- A reliable Mortgage Broker: To help you secure the best financing terms.

- A skilled Contractor: For accurate repair estimates and quality renovations.

- A professional Property Manager: To handle tenant screening, rent collection, and maintenance coordination if you choose to be a passive landlord.

Surround yourself with experienced investors. Join local real estate investment associations (REIAs), listen to podcasts, and read books. Learning from the mistakes of others is the cheapest education you will ever get.

Overcoming Analysis Paralysis and Taking Action

At the end of the day, the most important step in real estate investing is simply to start. Many beginners fall into the trap of “analysis paralysis.” They spend years reading books, listening to podcasts, and running hypothetical numbers without ever actually making an offer. They are terrified of making a mistake, so they do nothing at all, which guarantees they will miss out on years of potential wealth creation.

You do not need to buy a massive 50-unit apartment complex on your first try. Start small. Try house hacking a duplex, buy a modest single-family rental in a stable neighborhood, or simply open a brokerage account and buy your first shares of a REIT. The goal of your first deal is not to get rich overnight; the goal is to gain experience, learn the process, and build your confidence.

You will make mistakes. You might overestimate repair costs or underestimate the time it takes to find a tenant. That is completely normal. The key is to take calculated risks, learn from those mistakes, and scale up over time. Once you take that first step and close your first deal, the abstract concepts of real estate will transform into practical, tangible reality.

Conclusion

Real estate does not have to be an exclusive club reserved for the ultra-wealthy or those with decades of experience. Whether you choose to build sweat equity through house hacking, generate passive income through traditional rental properties, or invest hands-off via REITs, there is a strategy that fits your financial situation and lifestyle. By understanding the core pillars of wealth creation, setting clear goals, running rigorous mathematical analysis, and building a strong team, you can successfully navigate the market. The journey to financial freedom through property begins with a single step. Educate yourself, analyze the numbers, and take action today to build your long-term wealth.

Frequently Asked Questions (FAQ)

1. How much money do I need to start investing in real estate?

The amount of money required depends entirely on the strategy you choose. If you invest in Real Estate Investment Trusts (REITs), you can start with as little as $100 to buy shares on the stock market. For physical real estate, utilizing an FHA loan for “house hacking” allows you to buy a multi-family property with a down payment as low as 3.5%. Traditional investment property loans usually require 20% to 25% down. Therefore, you can start with very little capital if you utilize the right financing strategies or start with REITs.

2. What is the best real estate strategy for absolute beginners?

For beginners with limited capital and a desire to learn the ropes, “house hacking” is widely considered the best strategy. By buying a duplex or triplex, living in one unit, and renting out the others, you can qualify for a low-down-payment primary residence loan while offsetting your living expenses. It provides a gentle introduction to being a landlord since you live on the property. For those who want zero involvement, investing in REITs is the best beginner-friendly passive strategy.

3. How do I evaluate if a rental property is a good investment?

You must evaluate a property strictly by the numbers, not by its aesthetics. Calculate the expected monthly rent and subtract all operating expenses, including the mortgage (PITI), property taxes, insurance, property management fees, and allowances for vacancy and capital expenditures (repairs). If the property generates positive cash flow after all these expenses, and meets your target return metrics (like Cash-on-Cash return or the 1% rule), it is a good investment. Always run conservative numbers to ensure the deal works even if things go wrong.

4. What are the primary tax benefits of investing in real estate?

Real estate offers significant tax advantages. The most notable is depreciation, which allows you to deduct the cost of the building (not the land) over 27.5 years, creating a “paper loss” that can offset your rental income, thereby reducing your taxable income. Additionally, you can deduct ordinary and necessary expenses for managing and maintaining the property, including property management fees, repairs, insurance, and mortgage interest.

5. Can I invest in real estate without becoming a landlord?

Yes, absolutely. If you do not want to deal with tenant calls, repairs, and evictions, you have two main options. First, you can invest in Real Estate Investment Trusts (REITs), which allow you to buy shares of large-scale real estate portfolios on the stock market, providing dividend income with zero management responsibility. Second, if you buy a physical property, you can hire a professional property management company to handle all tenant-related issues and maintenance for a percentage of the monthly rent, making your investment largely hands-off.